Attachment of earnings

An attachment of earnings means a creditor levies an attachment to the salary of an employee (debtor), so that the debt is paid through the salary. Because part of the paid salary goes directly to the creditor, less money is paid out to the employee. The employer is obliged to cooperate with an attachment if the creditor (or bailiff) have complied with all the legal requirements.

Video

Description

If you receive an attachment of earnings (generally from a bailiff), you record it against the employee. The bailiff will supply you with the following data:

Per employee per period, Profit determines if there are attachments of earnings. If so, Profit first determines the 'repayment capacity'. This is a part of the payable wage from which repayments can be deducted. If Profit needs to apply a personal allowance, Profit also applies the 'personal allowance correction'. The 'correction for the personal allowance' is a calculation basis that includes the net expense allowances (attachments of earnings are not allowed to be applied to these types of wage components).

Repayment capacity = Payable wage -/- Personal allowance -/- Personal allowance correction

Example:

An employee has a payable wage of 2,000.00. The payable wage includes a net expense reimbursement of 100.00.

He has a preferential attachment of earnings in period 1 van 3,000.00 (personal allowance 1,000.00).

Repayment capacity = 2,000.00 -/- 1,000.00 -/- 100.00 = 900.00

Profit deducts the maximum repayment per period until the entire attachment of earnings is paid off.

Period

|

1

|

2

|

3

|

4

|

Wages to be paid

|

2,000

|

2,000

|

2,000

|

2,000

|

Repayment capacity

|

900

|

900

|

900

|

900

|

Repayment

|

900

|

900

|

900

|

300

|

To receive

|

1,100

|

1,100

|

1,100

|

1,700

|

You can also record an attachment of earnings in the form of a payment arrangement in Profit. In case of a payment arrangement, Profit repays a fixed amount per period. If the residual amount in the last period is lower than the default repayment, Profit only repays the residual amount. As a result, the attachment of earnings falls to zero. If only a periodic attachment of earnings is in force, Profit does not apply a personal allowance.

Example:

An employee has a payable wage of 2,000.00.

He has an attachment of earnings of 3,575.00 with a periodic repayment van 900.00.

Period

|

1

|

2

|

3

|

4

|

Wages to be paid

|

2,000

|

2,000

|

2,000

|

2,000

|

Repayment

|

900

|

900

|

900

|

875

|

To receive

|

1,100

|

1,100

|

1,100

|

1,125

|

In specific periods, the payable wage can be higher because of, for example, the holiday allowance or an annual bonus. This, of course, means that the repayment of a preferential attachment of earnings should also be higher. This is not the case with a periodic attachment of earnings, because the repayments are the same in each period.

More information:

Multiple attachments of earnings in the same period

Multiple attachments of earnings in the same period

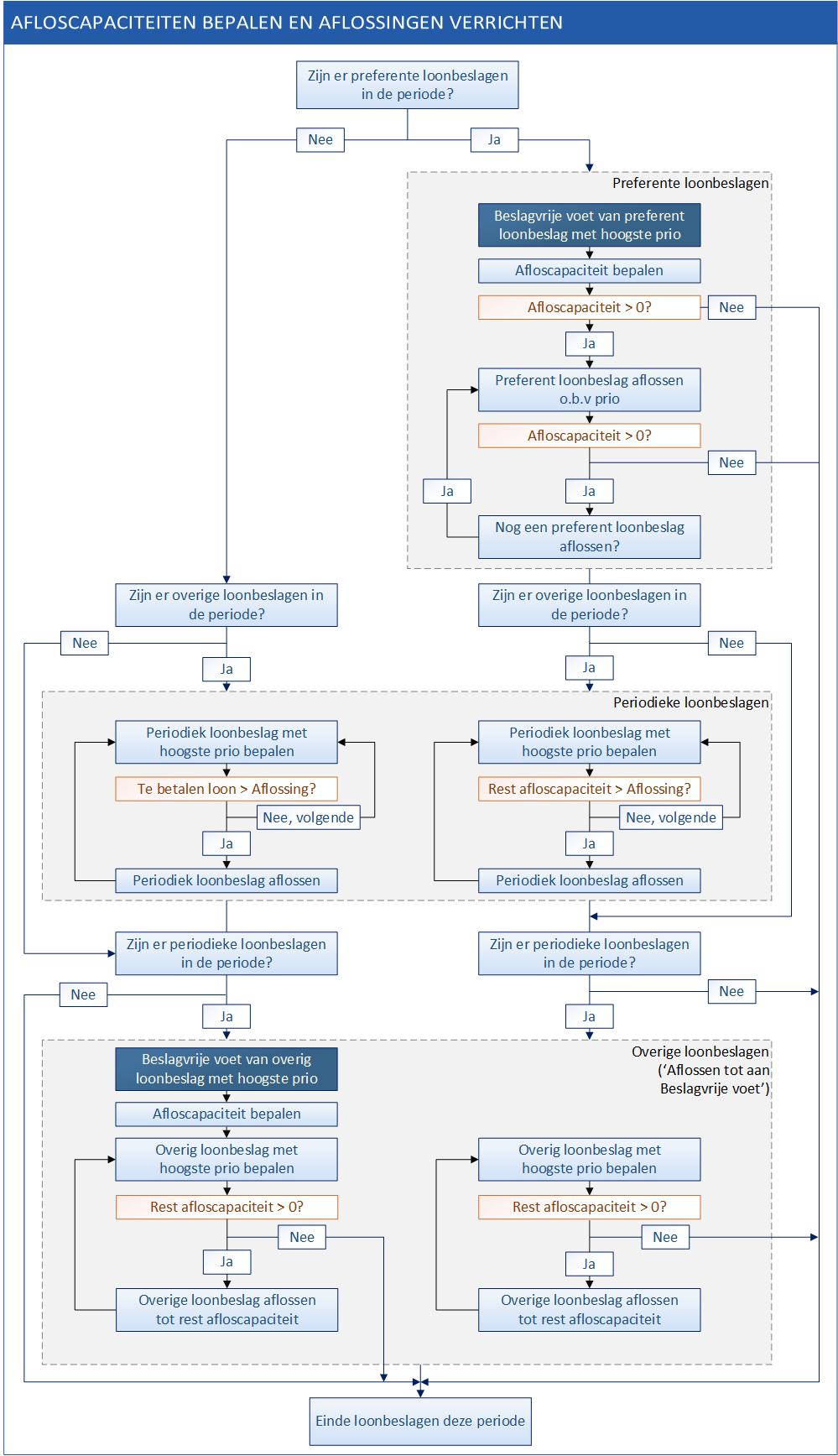

The table contains the types of attachments of earnings that you can record in Profit, in decreasing order of priority. If multiple attachments of earnings are in force in a single period, Profit determines the attachment of earnings to be repaid first on the basis of the priority of the attachments of earnings. Generally, this attachment of earnings will consume the entire repayment capacity which means that other attachments of earnings are not considered. However, sometimes the repayment capacity is large enough for the repayment of multiple attachments of earnings (in order of priority) in one period.

Type

|

Priority

|

Repayment amount

|

Preferential

|

Has the highest priority and will therefore be repaid first.

In case of two attachments of earnings of this type, the attachment with the oldest start date has priority. Only when this is completely repaid does the next attachment of earnings follow.

|

Entire repayment capacity until the debt is completely repaid.

|

Periodic repayment

|

Only repaid if there is still repayment capacity after the repayment of preferential attachments of earnings

Profit repays a periodic repayment only if the period amount can be deducted completely. If the repayment capacity is too low for this, no deduction takes place. Profit then goes on to the next periodic attachment of earnings (if this attachment has a lower period amount, it can perhaps be repaid).

In case of two attachments of earnings of this type, the attachment with the oldest start date has priority.

|

Fixed amount per period.

If a preferential attachment of earnings with a personal allowance falls in the period, the personal allowance also applies to the periodic repayment. If a periodic repayment amount is too high, Profit does not perform the repayment.

If there is no preferential attachment of earnings, Profit performs one repayment per periodic attachment of earnings (unless this results in a negative wage).

|

Repay up to the personal allowance

|

Only repaid if there is still repayment capacity after the repayment of preferential attachments of earnings and attachments with periodic repayment.

In case of two attachments of earnings of this type, the attachment with the oldest start date has priority. Only when this is completely repaid does the next attachment of earnings follow.

|

Entire repayment capacity until the debt is completely repaid.

|

If an employee has multiple attachments of earnings in the same period, Profit determines the personal allowance as follows:

- If a preferential attachment of earnings occurs in a period, the personal allowance from the first preferential attachment of earnings also applies to all other attachments in this period (including periodic attachments and attachments of the Repay up to personal allowance tyoe).

- If there is no preferential attachment of earnings, there is no personal allowance for periodic attachments.

- If there is no preferential attachment of earnings but there are attachments of earnings of the Repay up to personal allowance type, the personal allowance for the first attachment of earnings also applies to all other attachments in this period.

Example: Combination of attachments of earnings

An employee has a payable wage of 2,000.00. The payable wage includes a net cost reimbursement of 100.00.

As from period 1, he has the following attachments of earnings:

- Preferential attachment of earnings of 3,000.00 (personal allowance 1,000.00).

- Periodic attachment of earnings of 2,100.00 in three instalments of 700.00.

- Attachment of earnings of the Repay up to personal allowance type of 1,000.00 (personal allowance 1,000.00).

Repayment capacity = 2,000.00 -/- 1,000.00 -/- 100 = 900,00

Profit deducts the maximum repayment per period until the entire attachment of earnings is paid off.

Period

|

1

|

2

|

3

|

4

|

5

|

6

|

7

|

8

|

Payable wage

|

2,000

|

2,000

|

2,000

|

2,000

|

2,000

|

2,000

|

2,000

|

2,000

|

Repayment capacity (based on the preferential attachment of earnings)

|

900

|

900

|

900

|

900

|

900

|

900

|

payable wage

|

n/a

|

1. Repayment of preferential attachment of earnings

|

900

|

900

|

900

|

300

|

done

|

done

|

done

|

done

|

2. Repayment of periodic attachment of earnings

|

0

|

0

|

0

|

0

|

700

|

700

|

700

|

done

|

3. Repay up to the personal allowance

|

0

|

0

|

0

|

600

|

200

|

200

|

done

|

done

|

To receive

|

1,100

|

1,100

|

1,100

|

1,100

|

1,100

|

1,100

|

1,300

|

2,000

|

Explanation:

- Profit begins with the preferential attachment of earnings. Thus, in period 1 -3, there is no repayment capacity for the other attachments of earnings.

- The residual of 300.00 from the preferential attachment of earnings is repaid in period 4. Thus, a 'residual capacity’ of 600.00 remains. Based on priority, the periodic attachment should be paid now but the periodic amount of 700.00 is too high. That is why Profit proceeds to the third attachment of earnings.

- In period 5, 6 and 7, Profit performs the periodic repayments. A personal allowance does not apply (because there is no longer a preferential attachment of earnings). Profit does however determine a personal allowance for the attachment of earnings of the Repay up to personal allowance type.

- In period 7, Profit no longer determines a personal allowance because now only a periodic attachment of earnings is active.

You can use the diagram to verify how Profit determines the repayment capacity and performs repayments if there are multiple attachments of earnings in the same period.

RAE entries for approved periods

New attachments of earnings or changes in an existing attachment never lead to RAE entries in approved periods. After all, payments in approved periods can no longer be changed. If the next non-approved period has already been processed, Profit applies RAE to this period.

If an RAE entry originates in an approved period for other reasons, the room for attachments of earnings increases or decreases:

- Room for attachment of earnings increases

This means that the attachment of earnings was too low. If the attachment of earnings in question is still active, the next deduction is raised.

Example:

An employee has a payable wage of 1,500.00 and an attachment of earnings of 10,000.00 with a personal allowance of 800.00.

During the processing of period 1, Profit deducts a repayment van 700.00 (all the room available).

A correction takes place for period 1, increasing the payable wage increase y 100.00. This means that Profit applies an attachment of earnings of 100.00 in the correction period.

As a result of a correction, the payable wage of an employee can rise above the personal allowance whereas previously it was under the personal allowance. This can then result in an extra repayment.

Example:

An employee has a payable wage of 600.00 and an attachment of earnings of 10,000.00 with a personal allowance of 800.00.

During the processing of period 1, Profit deducts nothing (after all, the employee earns less than the personal allowance).

A correction takes place for period 1 which means that the payable wage increases by 300.00. As a result, the total wages payable is 900 and there is now room for a repayment of 100.00. This means that Profit applies an attachment of earnings of 100.00 in the correction period.

- Attachment of earnings is lowered

If the attachment of earnings for an approved periods is lowered, Profit settles this in the correction period, assuming that the attachment of earnings is still active.

Example:

An employee has a payable wage of 1,500.00 and an attachment of earnings of 10,000.00 with a personal allowance of 800.00.

During the processing of period 1, Profit deducts a repayment van 700.00 (all the room available).

A correction in period 1 takes place, lowering the payable wage to 1,400.00. This means that 100.00 too much was repaid in period 1. The normal repayment for period 2 is 600.00 but Profit compensates for the 100.00 too much that was paid in period 1. This means that the repayment for period 2 is 500.00.

Employee is re-employed or changes employer

Profit keeps track of attachment of earnings per employee, regardless of the labour relation or the employment. If the employee leaves employment, Profit does not check for any current attachment of earnings. If the employee re-enters employment with the same or a different employer, then the current attachments of earnings automatically come into effect again. If this is not desirable, you will need to enter an end date in the properties of the relevant attachment of earnings.

Profit also deducts an active attachment of earnings if there is a back pay contract.

Change the attachment of earnings end date

If an attachment of earnings must be repaid completely, Profit deducts a repayment periodically until the principal sum is repaid in full. In the period of the last repayment, Profit automatically enters the end date and stops the attachment of earnings.

If you want to end the attachment of earnings early, you enter an end date. Profit performs the last deduction in the period of the end date.

If you change the end date, the following situations can arise:

- Extension of the attachment of earnings

The old end date was in an approved period but the new end date is in a provisionally processed period. In other words: you extend the period of the attachment of earnings up to and including the provisionally processed period. Profit applies RAE to this period.

- Shortening of the attachment of earnings

The old end date was in a processed period but the new end date is in the last approved period. In other words: you shorten the period of the attachment of earnings up to and including the approved period. Profit applies RAE to this period.

- Skip periods (pause in attachment of earnings).

You have entered an end date but after a few periods the attachment of earnings starts once again (you remove the end date). In the intervening periods, Profit does not apply the attachment of earnings.

Example:

A monthly paid employee completes an attachment of earnings in May and thus the end date is set to 31 May.

In September you decide to remove the end date because there is still an outstanding balance. This means that Profit will once again apply the attachment of earnings as from September, assuming this period is still not approved. In June, July en August, Profit does not apply the attachment of earnings.

Administrative premium 'Zorginstituut Nederland (CVZ)'

In Profit the administrative premium is not an attachment of earnings. You can enter the deduction on the 100.008.121 'Inhouding bestuursrechtelijke premie Zorginstituut Nederland (CVZ)' wage component.

Note:

Each wage component has a comment in which the operation of the wage component is explained. Always take a look at this explanation on the Comment tab in the properties of the wage component in the CLA. If you do not have the wage component available, first activate it.

Personal allowance at start or end of employment halfway through the period

The personal allowance is not calculated proportionally when the employee starts and ends his or her employment. The personal allowance is a master data item in Profit that cannot be calculated proportionally.

If you want a lower personal allowance, manually adjust the amount for the personal allowance. This could, for example, apply if the employee leaves employment midway through the period and therefore earns less.

Preparation

Procedure

Also see