'ZVW' refund for last year

Note:

Because we have deactivated the wage component 100.005.041 'Teruggaaf gedifferentieerde premie WGA vorig jaar' as of 2014, during the salary processing you may see a message indicating that a wage component could not be calculated. This probably refers to wage component 100.005.042 'Teruggaaf werknemersverzekeringen vorig jaar'. Because by default we deliver this wage component non-activated, the activation parameter of this wage component has a value at the customer level. You can deactivate this wage component as from 31-12-2013, because as a part of the ‘Wet Uniformering Loonbegrip’ the refund of the employee insurances no longer applies after the year 2013.

In exceptional cases, there may still be recalculations from 2012 or earlier. You can process these directly in the financial administration.

The refund regulation for the 'ZVW' of the previous year only applies to employees with at least two employers, because in that case they could end up paying more in 'ZVW' premium than the maximum amount, because the employers are not aware of each other's payments. The refund takes place once every year in the period in which the tax authority refunds the amount to the employer.

Wage components

In the Profit CLA and Basic CAO the following wage components are present for this purpose:

- 100.005.034 'ZVW Teruggave van teveel ingehouden bijdrage vorig jaar'

- 100.005.035 'ZVW Teruggave vorig jaar'

- 100.005.036 'ZVW Teruggave vorig jaar (saldering negatief)'

Note:

Each wage component has a comment in which the operation of the wage component is explained. Always take a look at this explanation on the Comment tab in the properties of the wage component in the CLA. If you do not have the wage component available, first activate it.

'ZVW' refund in Profit

The employer has to pay a mandatory 'ZVW' employer share that equals the 'ZVW' premium. This means that the ZVW' premium has not cost the employee anything, apart from the fact that 'Loonheffing' has been calculated over the 'ZVW' employer share. The 'ZVW' refund is therefore not paid to the employee. However, a fiscal correction is necessary.

The employer includes this fiscal correction in the period in which the tax authority pays the refunds. This creates the problem that an employee may have left employment already or that the fiscal correction results in a positive wage before 'Loonheffing'. If the employee is still employed and the value is lower than the wage before 'Loonheffing', this fiscal correction is included in the wage declaration. If that is not the case, this fiscal correction takes place using the income tax of the employee.

For both statuses, you perform a calculation in Profit. The difference between making a correction using the wage declaration or using the income tax, also means that the payroll statement is composed differently. You enter the amount to be refunded for the employee in question on the 100.005.034 'ZVW Teruggave van teveel ingehouden bijdrage vorig jaar' wage component via HR / Payroll / Enter wage entry. Because Profit automatically determines whether the correction is made using the wage declaration or the wage tax, you do not have to look at this.

Note:

For an employee who has left employment, you add a back pay contract to be able to enter the 'ZVW' refund for the previous year.

Operation of the 'ZVW Teruggave van teveel ingehouden bijdrage vorig jaar' wage component

On the 100.005.034 'ZVW Teruggave van teveel ingehouden bijdrage vorig jaar' wage component, you enter the amount that is paid to the employer by the tax authority. Depending on the situation, one of the following wage components is used in the wage calculation:

- 100.005.035 'ZVW Teruggave vorig jaar'

- 100.005.036 'ZVW Teruggave vorig jaar (saldering negatief)'

If an employee is no longer employed, is dead or does not have enough 'Loonheffing' wage in the payment period, the 100.005.036 'ZVW Teruggave vorig jaar (saldering negatief)' wage component is automatically used for the calculation because the payroll statement and the wage declaration are handled in a different way.

In this situation settlement occurs using the income tax declaration (every employee with at least two employers receives an income tax declaration form).

In other situations, the calculation takes place using the 100.005.035 'ZVW Teruggave vorig jaar' wage component.

Operation of the 'ZVW Teruggave vorig jaar' wage component

The 100.005.035 'ZVW Teruggave vorig jaar' wage component determines if the 'Loonheffing' over the value of the 'ZVW' that is being refunded can in fact, according to the regulations of the tax authority, be refunded to the employee using the salary administration. This is done based on the amount that has been entered on the 100.005.034 'ZVW Teruggave van teveel ingehouden bijdrage vorig jaar' wage component.

If settlement based on the 'Loonheffing' wage is not possible, the 100.005.036 'ZVW Teruggave vorig jaar (saldering negatief)') wage component is used in the calculation and the amount is processed as a negative wage with the intention that matters will be straightened out via the income tax.

Operation of the 'ZVW Teruggave vorig jaar (saldering negatief)' wage component

The 100.005.036 'ZVW Teruggave vorig jaar (saldering negatief)' wage component determines if the 'Loonheffing' over the value of the 'ZVW' that is being refunded is not allowed to be refunded to the employee using the salary administration on the basis of the regulations of the tax authority. This is done based on the amount that has been entered on the 100.005.034 'ZVW Teruggave van teveel ingehouden bijdrage vorig jaar' wage component.

If settlement can take place with the ‘Loonheffing’ wage, the 100.005.035 'ZVW Teruggave vorig jaar' wage component is used for the calculation.

If the 100.005.036 'ZVW Teruggave vorig jaar (saldering negatief)' wage component is corrected in the last period of the year without any changes being made, you process this correction as follows:

- Employee is still employed

If the value of the correction is less than the 'Loonheffing’ wage, this tax correction can be performed using the wage declaration. If it is not, then this tax correction must be processed using the ‘IB’ declaration of the employee.

- The employee is no longer employed

Settle the employee correction using the ‘IB’ declaration.

Sample calculations

Below are a number of sample calculations.

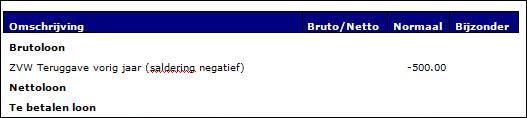

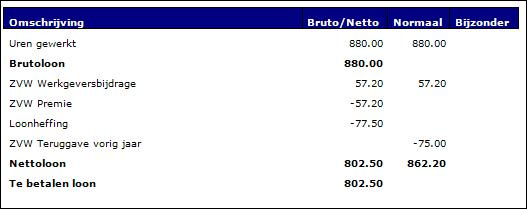

Sample calculation of 'ZVW' refund:

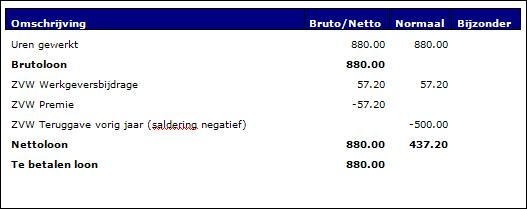

Sample calculation of 'ZVW' refund larger than 'Loonheffing' wage:

Sample calculation of 'ZVW' refund in case of a back pay contract: